The housing market may be heading for a slowdown based on rising home process and a jump in mortgage interest rates according to some industry experts.

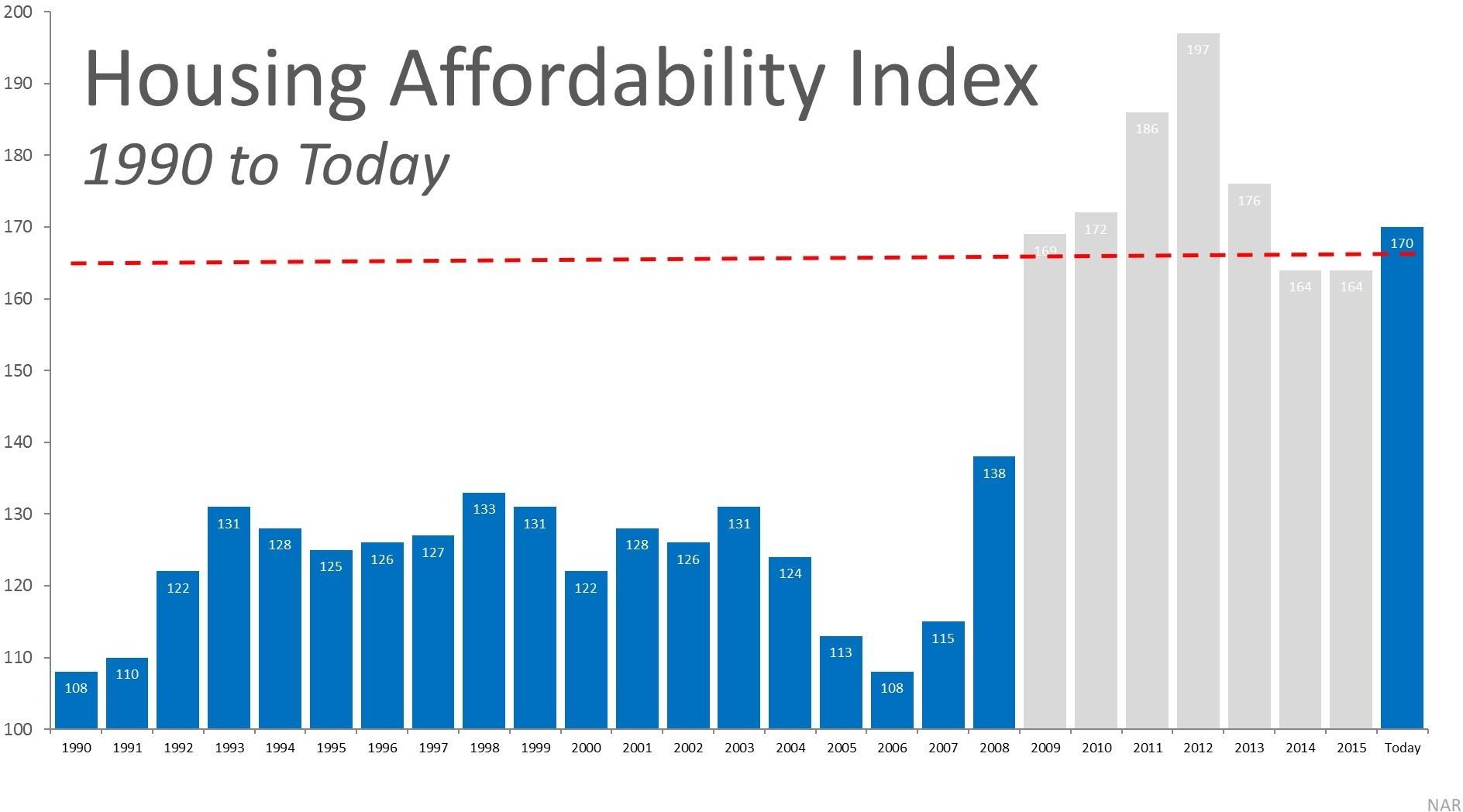

One of the data points they used is the Housing Affordability Index.

According to the National Association of Realtors (NAR), the index measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national level based on the most recent price and income data.

What this means is a value of 100 indicates a family earning the median income and is qualify enough for a mortgage on a median-priced home based on the price and mortgage rates at that time.

The family has more than enough to qualify if their score is anything above 100. The higher index tells us that it is easier for a family to afford a home.

Some are concerned about the decline of the index over the last several years as home values increased. But you should not be worried about it.

The housing crises from 2009 through 2013 left the market with an overabundance of housing inventory. One of the three listings was a distressed property (foreclosure or short sale).

All prices dropped and distressed properties sold at major discounts. Thus, mortgage rates fell like a rock.

Here’s good news for you. The market is recovering and values are coming back nicely. These have caused the index to fall.

If we remove the housing crisis years and look at the current index and compare it to the index from 1900 to 2008, we can see that mortgage rates are still lower than historical averages.

They’ve put the index in a better position than every year for the nineteen years before the crash.

The Housing Affordability Index should not be seen as a challenge to the real estate market’s continued recovery. It is in great shape!